2015-08-21

2015-08-21 534

534In 2008 several new issues emerged in the Kazakh banking sector, which together have become the dominant factor shaping the financial system as a whole. Among the most significant current trends are:

Ø a sharp decline in the rate of growth of the banking system;

Ø a significant weakening of asset quality;

Ø a decline in profitability at Kazakh banks.

5. http://www.globalissues.org/article/768/global-financial-crisis#Asiaandthefinancialcrisis

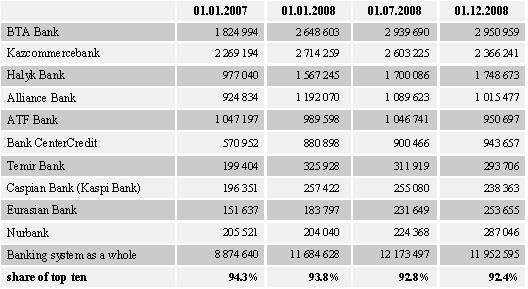

In order to provide a clearer illustration of these trends, let us have a look on Kazakhstan’s top ten banks (which together account for 92.4% of the banking systems assets) rather than just looking at the banking system as a whole (see Table 1).

Table 1. Assets at Kazakh banks* (mln tenge)

Growth at Kazakh banks is not what it was. Following a period of rapid expansion – driven mainly by international borrowing – the rate of growth for the banking system as a whole fell from 31.6% in 2007 to 2.3% in the 11 months of 2008. Moreover, by early December of 2008 total assets declined by 1.8% compared to the first half of the year.

The global liquidity crisis has plainly cut Kazakh banks off from further access to relatively low-cost international funding.

At the same time, the total volume of external obligations remains high. Despite the fact that the total external debt decreased by 10% in 2008, given the domestic market’s limited liquidity, KzRating sees re-financing as the only medium-term option for Kazakh banks in order to avoid cash shortfalls as they pay back existing non-resident loans.

Refinancing these obligations was the main challenge facing Kazakh banks in late 2007- early 2008. Asset quality has now emerged as a bigger issue.

Declining asset quality at commercial banks is in large part an outcome of the credit boom that lasted until the onset of the global crisis. Many banks relaxed lending requirements in their rush to invest resources drawn from outside the country. The cost of that liberalism is now becoming apparent. As long as the volume of loans continued to grow assessing their quality was difficult – the flow of new standard loans offset problems with existing assets. When the run of growth ended, however, banks found themselves looking at a decline in loan quality.

Even so, actual loan quality remains an open question in the case of corporate credit, where banks can manipulate the reported volume of problem loans, particularly in cases where funds are extended to affiliated or otherwise “friendly” companies. The formation of loan loss reserves has a direct impact on net revenues. As asset quality weakens, this has had an increasingly visible impact on earnings performance and, moreover, on the banking system as a whole.

Kazakh banks report a significant decline in net revenues. Compared to the first half of 2008, net income for the banking system as a whole decreased by half.

Besides forming provisions, falling returns reflect a rising cost of funds. The global crisis has forced larger banks to re-finance international borrowing at higher rates, while all banks face increasingly tough competition for access to domestic resources, which have become more attractive to the major players. The banks themselves are pushing up interest rates in their home market as they seek to draw on domestic resources to meet obligations to non-resident creditors.

From the perspective of foreign investors this is clearly a positive development, but the Kazakh market simply lacks the resources to fully offset international borrowing, a situation that is not expected to change in the near future. This implies that profitability measures will continue to be driven by two main factors: the need to form reserves against weakening assets and the cost of funds on international markets.

Even though the government has signaled a willingness to be involved with creating a negotiating mechanism for foreign investors, the banks themselves have absolutely refused to consider any form of renegotiation, indicating their own confidence to pay off external debt. This is similar to the situation that occurred at the end of 2007 when the Kazakh government established liquidity lines for the banks, but set the costs so high that none of the banks used the resource. However, as one banker pointed out to us, the existence of a safety net promotes confidence and enables other, more market-oriented, bridging mechanisms to be established.

In summary: as the global recession deepens, the pressures will increase – Kazakh banks will need to refinance external debt, either from the external sources, from the internal market, and from the Kazakh government. The internal market is too small; the Kazakh government has sufficient foreign currency, and although the government has supported the banks, it seems unlikely that the government would use its entire reserve just to do this. Foreign investors have demonstrated a willingness to take Kazakh risk even during the global crisis, and so this source of credit is not closed – for refinancing new debt. Consequently, the banking sector will shrink, its profitability will continue to decrease, and asset quality will appear to decrease as non-performing loans increase in proportion to good loans (which get paid off). The pressures will be highest for the small banks, as the large banks compete for their domestic funding sources, but they do not have any foreign borrowings. Kazakhstan has demonstrated awareness that its banks and largest borrowers must retain a good credit history internationally, and so if the government needs to choose between which banks to help and which to let go, the banks with the highest international profiles will be given most favored status.

Overall, KzRating takes the view that although the Kazakh banks share a cold and skeptical investor sentiment with financial institutions around the world, the Kazakh government, regulator and banking sector are managing the systemic problems in a calm and flexible manner. The Kazakh approach has so far been successful, in that investors have come forward to refinance debt and not one bank has suffered from depositor panic or failed – a record not shared by all developed economies. [6]