2015-09-06

2015-09-06 962

962UNIT TWO

| SUPPLY. THE LAW OF SUPPLY ELASTICITY OF SUPPLY |

LEARNING OBJECTIVES

After studying this unit, you should be able to:

· define the notions of demand, supply, the law of supply, supply curve, supply schedule, elasticity of supply, elastic supply, inelastic supply, quantity supplied;

· state the role of supply as one of the key economic concepts;

· define the terminology related to supply;

· distinguish between supply and quantity supplied, elastic and inelastic supply;

· outline the main non-price determinants of supply.

STARTING UP

Task 1. А)Choose the correct alternative in order to get the definition of “supply”.

Supply is a fundamental economic definition/ concept that describes the total amount of a specific/special good or service that is available to sellers/consumers. Economists describe demand/ supply as the relationship between the quantity of a good or service sellers will offer for sale and the price charged for that good.

В) Give your arguments.

ü Is supply important? Why?

ü What concept is the opposite to supply?

Task 2. Using the expressions from the table given on page 8, comment on the following quotations.

ü Teach a parrot the terms “supply” and “demand” and you've got an economist. (Thomas Carlyle)

ü There is a supply for every demand. (Florence Scovel Shinn )

ü Supply always comes on the heels of demand. (Robert Collier )

TEXT

Transactions require both buyers and sellers. Unlike demand that describes the behaviour of consumers supply refers to the behaviour of sellers. Thus, demand is only one aspect of decisions about prices and the amounts of goods traded, the other is supply. In economics, supply relates to the quantity of goods or services that a producer or a supplier is willing to launch into the market at a particular price in a given time period, all other things being equal.

The law of supply states that the quantity of a commodity supplied varies directly with its price, all other factors that may determine supply remaining the same. The law of supply expresses the relationship between prices and the quantity of goods and services that sellers would offer for sale at each and every price. In other words, the higher the price of a product, the higher the quantity supplied.

Clearly the law of supply is the opposite to the law of demand. Consumers want to pay as little as they can. They will buy more when there is a price decrease in the market. Sellers, on the other hand, want to charge as much as they can. As the price goes up they will be willing to make more and sell more maximizing their profits.

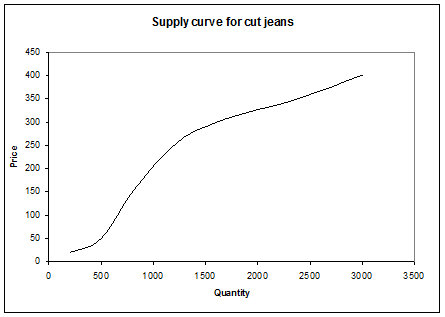

The relationship between the price of a product and its quantity supplied is represented in a table called a supply schedule. The supply curve is a graphical representation of the market supply schedule and the law of supply. The supply curve shows a direct relationship between the quantities of products that firms are willing to produce and sell at various prices, all non-price factors being constant.

Supply schedule for cut jeans

| Price | The quantity supplied |

| $400 | |

| $350 | |

| $300 | |

| $225 | |

| $175 | |

| $100 | |

| $50 |

The supply curve enables producers to anticipate what the supply would be for those prices falling in between the prices that are in the supply schedule. Each point along the curve represents a different price-quantity combination, or to put it another way, a direct correlation between the quantities supplied and price.

People often confuse supply with the quantity supplied. The difference between supply and quantity supplied is that

ü Supply represents the amounts of items that suppliers are willing and able to offer for sale at different prices at a particular time and place, all non-price determinants being equal.

ü The quantity supplied refers to the amount of a certain product producers are willing to supply at a certain price. A change in the price of the product will cause a change in the quantity supplied.

Price is an important determinant of the quantities supplied. The law of supply states that the amount offered for sale rises, as the price is higher. However, there are things other than price which affect the amounts of goods and services suppliers are able to bring into the market. These things are called the non-price determinants of supply. They are:

ü Changes in the cost of production. Production costs relate to the labour costs and other costs of doing business used in production process.

ü Changes in technology. Changes in technology usually result in improved productivity. Improved technology decreases production costs and therefore increases supply.

ü Changes in the price of resources needed to produce goods and services. If the price of a resource used to produce the product grows, this will increase the production costs and the producer will no longer be willing to offer the same quantity at the same price. He will want to charge a higher price to cover the higher costs.

ü Changes in the expectations of future prices. Changes in producers' expectations about the future price can cause a change in the current supply of products. If producers anticipate a price rise in the future, they may prefer to store their products today and sell them later. As a result, the current supply of a particular product will decrease.

ü Changes in the profit opportunities. If a business firm produces more than one product, a change in the price of one product can change the supply of another product. Profit opportunities encourage producers to produce those goods that have high prices.

ü Changes in the number of suppliers in the market. Potential producers are producers who can make a product but don’t do it because of relatively low price. If the price of a product rises potential suppliers will switch over productionto that product to make more profit.

An important concept in understanding supply and demand theories is elasticity. Elasticity of supply is a measure of how much the quantity supplied of a particular product responds to a change in the price of that product. It works similar to elasticity of demand. Supply is elastic if a change in price results in a large change in the quantity supplied while, if a great change in price brings about a small change in the quantity supplied, supply is called inelastic.

Making a summary it is necessary to emphasize that the understanding of concepts of supply and demand provides an explanation of how prices are determined in competitive markets.

ESSENTIAL VOCABULARY

1. Anticipate v –to imagine or expect that something will happen – передбачати, очікувати, сподіватися. Syn. to expect, to hope, to predict, to foresee.

2. Charge v –to impose or ask somebody for an amount of money as a price or fee – призначати, вимагати плату, правити. To charge/to establish/to fix/to set a price – призначати ціну.

3. Launch v – introduce a new product to the public for the first time – випускати на ринок (товар). Syn. tobring into the market.

4. Supplier n –a company or a person that provides things that people want or need, especially over a long period of time – постачальник. Syn. a provider, a producer, a seller.

5. Supply v –to make available something that is wanted or needed by somebody or something often in large quantities and over a long period of time – постачати, доставляти, надавати, задовольняти. Syn. to furnish, to provide, to sell.

6. Switch (from something to something) v - to change suddenly or completely, especially from one thing to another, or to exchange by replacing one thing with another – переміщати, міняти, змінювати. To switch over production –переключитися на виробництво/змінювати напрям виробництва. Syn. to shift, to transfer.

7. Transaction n –a business deal or agreement/ the action or process of buying or selling something – операція; угода. Syn. a bargain, a deal, an arrangement.

VOCABULARY EXERCISES